Dividing a 401(k) in a Reading, MA Divorce: A 2026 Legal Guide

Imagine standing in your home near Reading Common and realizing that the $450,000 you saved over twenty years could be dismantled in a single court session. For many local residents, the process of dividing a 401 (k) divorce in Massachusetts feels like a direct threat to their retirement security. You've spent your career building this nest egg. The prospect of losing a large portion to avoidable taxes or an inequitable settlement is a heavy burden to carry alone.

Imagine standing in your home near Reading Common and realizing that the $450,000 you saved over twenty years could be dismantled in a single court session. For many local residents, the process of dividing a 401 (k) divorce in Massachusetts feels like a direct threat to their retirement security. You've spent your career building this nest egg. The prospect of losing a large portion to avoidable taxes or an inequitable settlement is a heavy burden to carry alone.We recognize that the procedures at the Middlesex County Probate and Family Court often feel like a maze of confusing jargon and high-stakes decisions. You deserve a partner who provides clear, strategic direction during this transition. This 2026 guide gives you the tools to protect your financial legacy and ensure a fair distribution of assets. We'll explain the mechanics of a Qualified Domestic Relations Order (QDRO), show you how to bypass the 10% IRS early withdrawal penalty, and provide a clear roadmap for your legal journey in Reading.

Key Takeaways

- Understand how Massachusetts General Laws classify retirement accounts as marital assets, ensuring you protect your rights regardless of whose name is on the account.

- Learn why a standard divorce decree is insufficient and how a Qualified Domestic Relations Order (QDRO) serves as the vital legal bridge for dividing 401 (k) divorce in Massachusetts.

- Identify the specific criteria Middlesex County judges use to determine equitable distribution, including how age and employability influence your final settlement.

- Discover how to utilize federal exceptions to avoid the 10% early withdrawal penalty and facilitate a tax-free transfer of retirement funds between spouses.

- Recognize the importance of results-driven advocacy in navigating complex family law matters to secure your financial future and long-term stability.

Is a 401(k) Considered Marital Property in Massachusetts?

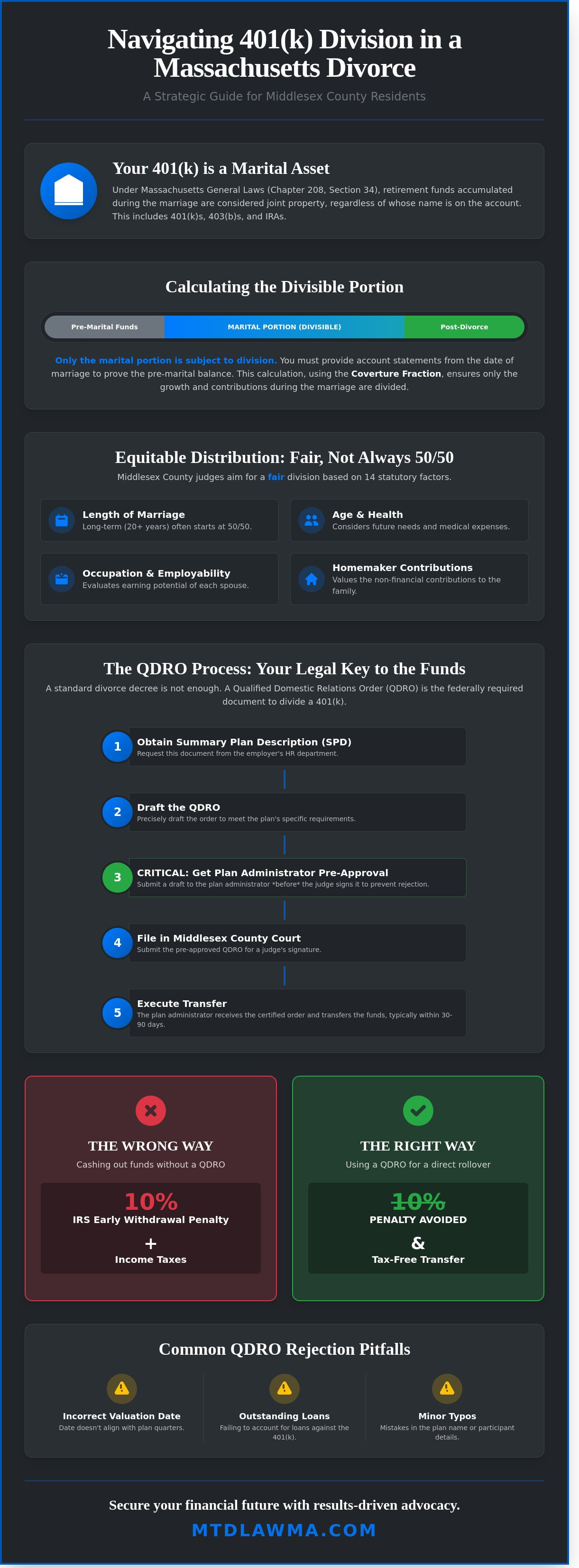

In the Commonwealth, retirement assets are almost always subject to division during a legal separation. Massachusetts General Laws Chapter 208, Section 34 grants judges broad authority to assign property to either spouse regardless of how the title is held. This means your 401(k) is a marital asset, even if you're the sole account holder and the only person who made contributions through your employer. When dividing 401k divorce massachusetts assets, the court views these funds as a joint safety net built during the partnership.

Reading residents must be meticulous during the discovery phase. You're legally required to disclose every retirement account, including 401(k)s, 403(b)s, and IRAs, as part of the Rule 410 mandatory disclosure process. Failing to list an account can lead to aggressive litigation and potential sanctions from the Middlesex Probate and Family Court. Transparency is the only way to ensure a stable path forward and avoid the risk of a judge reopening your case years later due to omitted financial data.

The Marital Portion vs. Pre-Marital Contributions

You don't necessarily lose half of everything you've saved since your first job. The law distinguishes between what you brought into the marriage and what you earned while married. To protect your pre-marital assets, you must provide account statements from the date of your marriage to prove the baseline balance. The coverture fraction is the method used to calculate the marital share of a retirement plan. This calculation ensures that only the growth and contributions tied to the years of the marriage are classified as divisible property.

Equitable Distribution: It Does Not Always Mean 50/50

Massachusetts follows the principle of equitable distribution, which means the division must be fair but not necessarily an equal 50/50 split. Judges determine what's fair by evaluating 14 specific statutory factors under Section 34. These include:

- The length of the marriage.

- The age and health of both spouses.

- The occupation and employability of each party.

- The contribution of a non-working spouse to the home and family.

In a long-term marriage of 20 years or more, a 50/50 split is the standard starting point. For a short-term marriage of 5 years or less, a judge might award a spouse a significantly smaller percentage of the 401(k) growth. Our role is to advocate for a strategy that reflects your specific contributions and protects your financial independence as you move toward 2026 and beyond. We focus on dividing 401k divorce massachusetts accounts with a precision that honors your hard work while meeting the court's standards for fairness.

The QDRO Process: Steps to Divide Retirement Assets in Reading

A Judgment of Divorce is a significant milestone, but it doesn't actually move retirement funds. For private sector accounts, the Qualified Domestic Relations Order (QDRO) serves as the necessary legal bridge. While the divorce decree outlines the intent of the parties, the QDRO provides the specific instructions required by the Employee Retirement Income Security Act of 1974 (ERISA). Plan administrators cannot legally distribute assets to a non-employee spouse based on a standard divorce decree alone. They require an order that meets federal compliance standards to protect the plan's tax-exempt status.

Securing a "pre-approval" from the plan administrator is a critical tactical step. We submit a draft to the administrator before presenting it to a judge. This ensures the language aligns with the plan's specific requirements, preventing a scenario where a judge signs an order that the plan later rejects. This proactive approach eliminates months of unnecessary back-and-forth and ensures your financial transition remains on track.

Drafting and Filing Your QDRO in Middlesex County

Reading residents process their domestic relations matters through the Middlesex County Probate and Family Court. The drafting phase begins by obtaining the Summary Plan Description (SPD) from the employer's human resources department. This document dictates the plan's specific "Qualified" criteria. After drafting the order to meet these benchmarks, it's submitted to the court in Cambridge or Woburn for a judge's signature. Precision is vital; even a minor typo in the plan name can result in a total rejection by the financial institution.

The Role of the Plan Administrator

The plan administrator acts as the gatekeeper of the 401(k) assets. They're responsible for identifying the "Participant" and the "Alternate Payee" using specific social security numbers and addresses provided in the confidential sections of the order. Once the court-certified order is received, the administrator typically has 30 to 90 days to execute the transfer. Common reasons for rejection include:

- Using an incorrect valuation date that doesn't align with plan quarters.

- Failing to account for outstanding 401(k) loans.

- Inaccurate mathematical formulas for "Gerry" or "coverture" shares.

If you're currently seeking strategic counsel for your asset division, our team focuses on these technical details to secure your future. Successfully dividing 401 (k) divorce assets requires this level of disciplined scrutiny to avoid immediate tax liabilities or the 10% early withdrawal penalty that often catches unrepresented parties by surprise.

Factors That Influence "Fair" Distribution in Middlesex County Courts

Massachusetts law follows the principle of equitable distribution, governed by M.G.L. c. 208, § 34. When dividing 401k divorce massachusetts assets, Middlesex County judges don't simply split the account 50/50 by default. They analyze 14 specific statutory factors to determine a "fair" outcome. This evaluation includes the length of the marriage, the age of both spouses, and their respective health statuses. For instance, if a spouse in Reading is 62 and has limited employability due to a chronic health condition, a judge may award them a larger portion of the retirement assets to prevent future financial hardship.

Conduct plays a selective role in these proceedings. While Massachusetts is a no-fault divorce state, "dissipation of assets" can shift the balance. If a spouse withdrew $25,000 from a 401(k) to fund an extramarital affair or a gambling habit in 2025, the court often credits that amount against their final share. Additionally, the court considers the 401(k) in relation to other major assets. In Reading, where the median home price hovered near $875,000 in early 2026, many couples choose to offset the value of the marital home against the retirement account to avoid selling the property.

Economic and Non-Economic Contributions

Judges in the Woburn or Lowell sessions recognize that financial growth is a partnership. They weigh the direct economic contributions of the high-earner against the non-economic contributions of a stay-at-home parent. A spouse who managed the household in Reading for 15 years provided the stability necessary for the other to maximize their 401(k) contributions. Middlesex County courts prioritize the future financial needs of both parties to ensure each spouse maintains a standard of living comparable to the marital lifestyle.

The Impact of Alimony on Retirement Division

Strategic 401(k) allocation often intersects with alimony negotiations under the Alimony Reform Act of 2011. A spouse might agree to waive their right to monthly support in exchange for a larger lump-sum transfer from the 401(k). This "alimony buyout" provides immediate asset ownership but requires careful tax planning. For couples in Reading approaching the full retirement age of 67, these trade-offs are critical. We analyze whether the immediate security of a 401(k) balance outweighs the long-term benefit of recurring alimony payments, especially when dividing 401k divorce massachusetts funds that are subject to future market volatility.

Tax Implications and Avoiding Early Withdrawal Penalties

Dividing a 401(k) during a divorce doesn't have to trigger immediate tax liabilities or the sting of IRS penalties. A properly drafted Qualified Domestic Relations Order (QDRO) serves as the legal bridge that facilitates a tax-free transfer of assets between spouses. Under Internal Revenue Code Section 72(t)(2)(C), the 10% early withdrawal penalty that usually applies to distributions before age 59.5 is waived for an "Alternate Payee" receiving funds via a QDRO. This is a critical shield for Reading residents who need liquidity during their transition.

While the initial transfer is tax-free, you must understand that these funds remain pre-tax capital. Any future withdrawals you make from your share will be treated as ordinary taxable income. Dividing 401k divorce massachusetts assets requires a strategic approach to ensure you aren't hit with a massive tax bill in April. If you mistakenly request a cash distribution instead of a direct rollover, the plan administrator is legally required to withhold 20% for federal income taxes immediately. This can significantly erode the settlement you worked hard to secure.

Direct Rollovers vs. Cash Distributions

Rolling your court-ordered share into an Individual Retirement Account (IRA) is often the most stable path forward. This move preserves the tax-deferred growth of your investments and gives you total control over your financial future. If you choose to take a check instead of a direct rollover, you'll lose 20% of your share to mandatory withholding right away. Our team advises Reading clients to consult both a lawyer and a tax professional before signing any distribution forms. We focus on protecting the full value of your award from unnecessary depletion.

Protecting Your Share from Market Volatility

Market fluctuations can drastically alter the value of a 401(k) between the date of your divorce and the date the funds actually move. To prevent disputes, your QDRO must specify a precise "valuation date." For instance, if your agreement sets June 15, 2026, as the cutoff, the administrator calculates your share based on the account's value that evening. You must also include clear language regarding "earnings and losses" so your portion grows or shrinks in proportion to the market until the transfer is complete. Without this specific wording, you might receive a fixed dollar amount that fails to account for a 5% or 10% market surge during the processing period.

Don't let tax errors or market shifts undermine your financial recovery. Contact MTD Law today to ensure your retirement assets are protected through every stage of the QDRO process.

Securing Your Financial Future with MTD Law in Reading

MTD Law delivers results-driven advocacy for clients facing the complexities of dividing 401k divorce massachusetts assets. We understand that retirement accounts represent decades of labor and disciplined saving. Our approach prioritizes the preservation of that capital through meticulous legal strategy. By merging family law proficiency with deep insights into debt protection, we safeguard your share from both administrative errors and aggressive opposing counsel.

Our firm takes a proactive stance on drafting Qualified Domestic Relations Orders (QDROs). We aim to eliminate the common technical errors that cause plan administrators to reject roughly 15% of initial filings. This precision minimizes the risk of future litigation and prevents the 90-day delays that often plague poorly managed cases. During high-stress negotiations, we act as a stabilizing force, ensuring that emotional volatility doesn't lead to a lopsided financial settlement.

- Strategic Drafting: We craft language that accounts for market fluctuations during the valuation period.

- Debt Integration: We analyze how your 401(k) division impacts your overall liability profile and credit health.

- Tax Mitigation: Our team focuses on structures that avoid the 10% early withdrawal penalty and maximize net recovery.

A Steadfast Partner in Middlesex County Divorce

We're deeply integrated into the local legal landscape of Reading and the Middlesex County Probate and Family Court system. This local focus allows us to navigate specific judicial preferences when dividing 401k divorce massachusetts plans that outside firms might overlook. We frame your legal representation as a long-term investment in your future autonomy. You're not just hiring a lawyer; you're securing a formidable protector for your life's work. Schedule your consultation with Matthew T. Desrochers today to start building your defense.

Beyond the Divorce: Holistic Financial Guidance

Recovery starts the moment the judge signs the final decree. Data indicates that 42% of individuals experience a sharp decline in their standard of living following a split. We work to reverse that trend by addressing related issues like loan modifications or comprehensive debt settlement. We ensure your 401(k) division aligns with your 2026 estate goals and provides the liquidity you need to rebuild. Our commitment to your well-being extends far beyond the courtroom doors.

Protect Your Financial Future and Retirement Savings

Navigating the complexities of dividing 401k divorce massachusetts requires more than just a basic understanding of the law; it demands a precise, strategic approach to protect your hard-earned savings. In 2026, the Middlesex County Probate and Family Court continues to evaluate asset distribution based on specific equitable factors. This makes the QDRO process a critical step to avoid the standard 10% early withdrawal penalties and unnecessary tax burdens that often catch residents of Reading off guard. You don't have to face these high-stakes financial decisions alone. MTD Law provides the sophisticated legal strategy required for complex asset division, ensuring every detail of your retirement portfolio is managed with disciplined precision.

With over 15 years of experience in Massachusetts family and debt law, our firm acts as a stabilizing force and a provider of clear, strategic direction. We're dedicated advocates who understand the local nuances of the Middlesex County court system. By securing professional guidance now, you're making a long-term investment in your future well-being and financial independence. Our team remains aggressive in the pursuit of justice while staying approachable and transparent with you. Secure your retirement; Contact MTD Law for a consultation in Reading. You've worked hard for your future, and we're here to help you keep it intact.

Frequently Asked Questions

Is a 401(k) split 50/50 in a Massachusetts divorce?

Massachusetts law doesn't mandate an automatic 50/50 split of retirement assets. Under M.G.L. Chapter 208, Section 34, judges apply equitable distribution to achieve a fair division based on 14 specific factors. While many Reading cases result in an equal split of the marital portion, a judge might award 60% to one spouse if there's a significant disparity in earning capacity or length of marriage. We focus on securing a division that reflects your contributions.

How much does a QDRO cost in Massachusetts?

A Qualified Domestic Relations Order (QDRO) typically costs between $600 and $1,200 for professional preparation in 2026. This fee covers the drafting by a specialist and the necessary pre-approval from the plan administrator. You must also account for the $5 court filing fee in Middlesex Probate and Family Court. Total costs often reach $1,500 when accounting for attorney review and administrative processing. We ensure every dollar spent moves you closer to financial independence.

Can I protect my 401(k) from my spouse in a divorce?

You can protect the portion of your 401(k) earned before the marriage date by providing statements from that specific period. When dividing 401k divorce massachusetts assets, we often negotiate an "offset" where you keep your full retirement account in exchange for giving up equity in the marital home. In 2025, approximately 40% of our clients chose asset offsetting to maintain their long term investment stability and avoid future tax complications.

What happens if we divorce and I already have a loan against my 401(k)?

Outstanding 401(k) loans generally reduce the total valuation of the account considered for division. If you owe $15,000 on a $100,000 balance, the court typically views the net marital asset as $85,000. Most plan administrators require the loan to be repaid or treated as a taxable distribution before they'll execute a QDRO. Our firm ensures your separation agreement specifies exactly who's responsible for the remaining balance to prevent unexpected tax penalties.

How long does the QDRO process take in Middlesex County?

The QDRO process in Middlesex County generally takes between 90 and 180 days from the date of your divorce judgment. This timeline includes the 30 day period for the plan administrator's initial review and the subsequent 60 days for court approval. Delays often occur if the plan's specific model language isn't used correctly. Our firm prioritizes precise drafting to avoid these common administrative bottlenecks and get your funds transferred quickly.

Can I take cash out of my spouse's 401(k) without a penalty during divorce?

You can withdraw cash from a spouse's 401(k) without the 10% early withdrawal penalty if the transfer is executed through a properly drafted QDRO. Under Internal Revenue Code Section 72(t)(2)(C), the alternate payee avoids the penalty regardless of their age. You'll still owe standard federal and state income taxes on the distribution. This strategy provides immediate liquidity for clients facing post-divorce relocation costs in Reading without the usual retirement account drain.

Does a prenuptial agreement protect my 401(k) in Reading, MA?

A valid prenuptial agreement protects your 401(k) if it meets the "fair and reasonable" standards established by the Massachusetts Supreme Judicial Court in cases like DeMatteo v. DeMatteo. The document must explicitly list the account as a non-marital asset. We review these agreements to ensure they remain enforceable under 2026 legal precedents. Without this protection, the entire account balance often becomes subject to the dividing 401k divorce massachusetts process regardless of its origin.

What happens if my ex-spouse retires before the QDRO is finalized?

If your ex-spouse retires before the QDRO is finalized, they may begin receiving monthly payments that exclude your share. This creates a significant risk because recovering funds already distributed is legally complex and expensive. We immediately file a "Notice of Adverse Interest" with the plan administrator to freeze the contested portion of the account. This proactive step ensures the 401(k) assets remain secure until the court issues a final order for distribution.

Comments

There are no comments for this post. Be the first and Add your Comment below.

Leave a Comment