Medical Debt Bankruptcy in Reading, MA: A Guide to Financial Recovery

We understand that a stack of balance billing statements and insurance denials represents a direct threat to your peace of mind. It's frustrating to feel like your hard-earned local assets are at risk because of circumstances beyond your control. This guide explains how Massachusetts bankruptcy laws can permanently discharge your medical bills and stop collection lawsuits immediately. We'll examine the specific protections available to Reading residents, including how to safeguard your home through the Homestead Act while achieving the fresh start you deserve.

Key Takeaways

- Identify how Massachusetts bankruptcy laws serve as a stabilizing force, allowing you to permanently discharge overwhelming medical bills and reclaim your financial independence.

- Compare the strategic advantages of Chapter 7 and Chapter 13 to determine the most effective path for liquidating arrears while protecting your assets in Reading.

- Navigate the complexities of medical debt bankruptcy reading ma with a localized checklist that covers everything from mandatory credit counseling to gathering records from Winchester Hospital.

- Dispel the misconception that filing for relief results in the loss of your doctor, ensuring you maintain essential healthcare access under state legal protections.

- Discover how dedicated legal advocacy provides a formidable shield against aggressive collectors, transitioning you from immediate crisis to long-term financial security.

The Reality of Medical Debt in Reading, MA

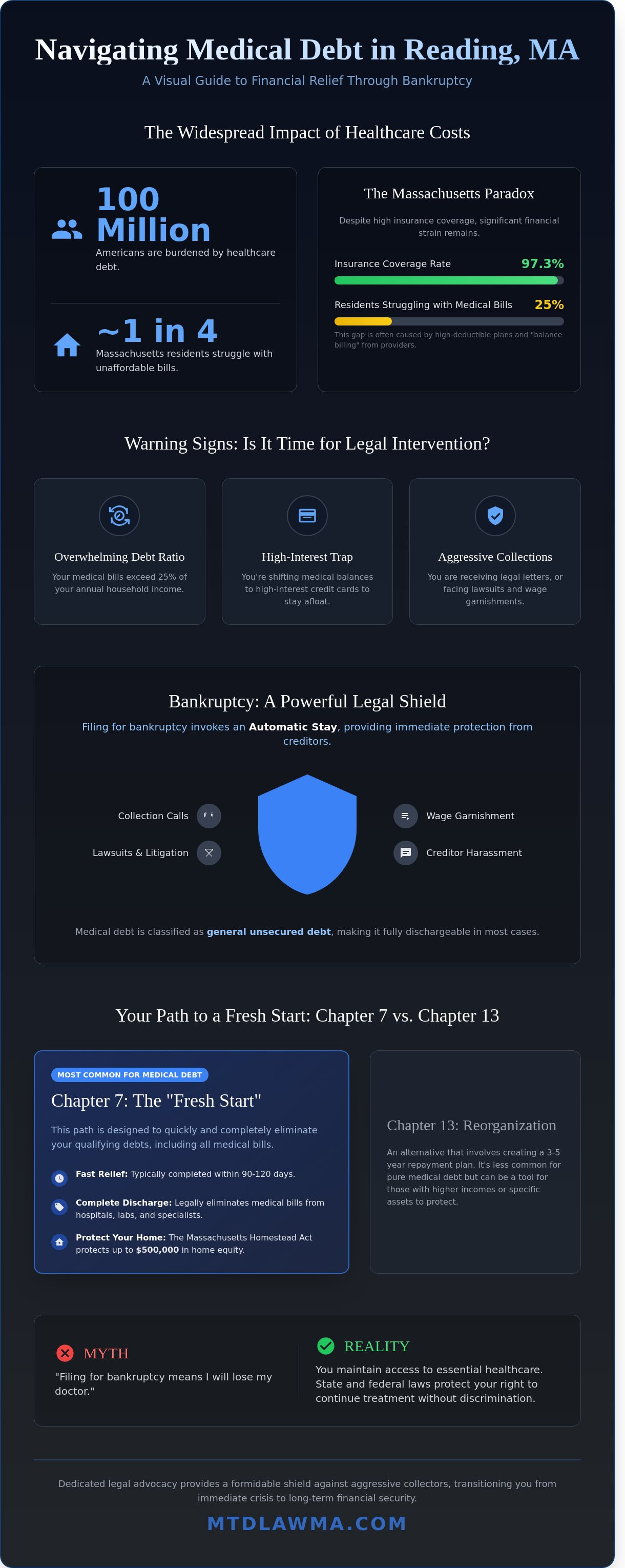

Medical debt remains the primary driver of personal insolvency across the Commonwealth. In Reading, families often fall into a specific trap known as the "Reading Gap." According to 2023 data from the Center for Health Information and Analysis (CHIA), Massachusetts maintains a 97.3% insurance coverage rate, yet nearly 25% of residents still struggle with medical bills they can't afford. Local providers like Beth Israel Lahey Health or Winchester Hospital eventually transfer delinquent accounts to third-party collectors. These agencies prioritize recovery over patient care, often ignoring the financial hardship of the debtor. Utilizing a strategy for medical debt bankruptcy reading ma allows you to pivot from a defensive posture to a proactive solution. This process halts collection actions and provides a definitive end to the cycle of mounting interest and harassment.

Medical debt bankruptcy is a specific application of the legal code designed to discharge healthcare-related liabilities and restore financial stability. By filing for relief, you invoke an automatic stay that prevents creditors from contacting you or pursuing litigation. It's not just a way to wipe the slate clean; it's a strategic tool for reclaiming your future. Our firm acts as a stabilizing force, ensuring that the complex rules of U.S. bankruptcy law work in your favor rather than against you.

Why Even Insured Residents in Reading Struggle

High-deductible health plans (HDHPs) have become the standard for many Middlesex County employers. These plans often require families to pay $6,000 or more out-of-pocket before coverage begins. You might also encounter "balance billing," where a provider charges you the difference between their fee and what the insurer pays. These costs accumulate rapidly during emergencies or chronic illness treatments. Under the framework of the bankruptcy code, medical debt is formally categorized as general unsecured debt. This classification is vital because it allows for full discharge in most Chapter 7 cases, treating the debt as a low priority compared to secured assets.

Signs Your Medical Debt Requires Legal Intervention

Financial distress often follows a predictable pattern. If your outstanding medical bills exceed 25% of your annual Reading household income, your recovery without legal assistance is statistically unlikely. Many residents try to bridge the gap by shifting medical balances to high-interest credit cards. It's a dangerous tactic that converts manageable medical debt into a high-interest trap with fewer consumer protections. You should also watch for aggressive collection tactics. Massachusetts-based agencies or local law firms specialized in debt recovery often use lawsuits or wage garnishments to force payment. When a hospital's billing department stops answering your calls and starts sending letters from a legal office, it's time to seek professional advocacy to protect your assets.

Chapter 7 vs. Chapter 13: Wiping Out Medical Bills

Choosing the right legal framework is the first step toward reclaiming your financial independence. Medical debt is classified as general unsecured debt, meaning it isn't backed by collateral like a home or a vehicle. Because of this classification, a medical debt bankruptcy reading ma filing is exceptionally effective. These obligations are almost always dischargeable, allowing you to legally extinguish balances from hospitals, specialists, and diagnostic labs.

Chapter 7: The Most Common Path for Medical Relief

Chapter 7 bankruptcy is often called a "straight" bankruptcy or a fresh start. It's the most frequent choice for individuals overwhelmed by healthcare costs because it works quickly. For Reading residents filing in 2026, eligibility is determined by the Means Test. This formula compares your average monthly income over the last six months to the Massachusetts median income. If your earnings fall below this threshold, you generally qualify for a full discharge of your medical liabilities.

The process is efficient. Most clients receive their discharge notice within 90 to 120 days of their initial filing. You don't have to worry about losing your residence during this time. The Massachusetts Homestead Act provides a robust safety net. While an automatic $125,000 protection exists, filing a formal Declaration of Homestead can protect up to $500,000 in home equity. This is a critical shield for homeowners in Reading where property values have seen steady growth. While recent updates to Massachusetts medical debt regulations help keep these bills off credit reports, they don't stop a provider from suing you. Bankruptcy provides the permanent injunction you need to stop all collection efforts.

Chapter 13: Reorganizing Debt for Long-Term Stability

If your income exceeds the limits for Chapter 7, Chapter 13 provides a strategic alternative. This chapter is designed for high-earners or those with significant non-exempt assets they wish to protect. Instead of a total liquidation, you'll propose a three to five year repayment plan. This plan is based on your disposable income rather than the total amount of debt you owe.

In the repayment hierarchy, medical debt sits at the bottom. Your plan first addresses "priority" claims, such as recent tax obligations or domestic support. Medical bills are grouped with other unsecured debts, and in many Reading cases, debtors pay back only a small fraction of the original balance. Once you complete the three to five year term, the court discharges any remaining medical arrears. If you're unsure which path secures your assets most effectively, speaking with an experienced advocate can provide the clarity needed to move forward. Our firm focuses on proactive, results-oriented strategies that turn complex legal hurdles into manageable recovery plans.

Medical Debt Myths vs. Massachusetts Legal Reality

Misconceptions often prevent residents from seeking the relief they deserve. You might feel that filing for bankruptcy is a sign of financial mismanagement. In reality, medical crises are the leading driver of insolvency in the United States. For those considering medical debt bankruptcy reading ma, it's vital to separate outdated stigmas from the current legal framework. Bankruptcy isn't a badge of irresponsibility; it's a strategic tool designed to protect your future from the weight of unmanageable healthcare costs. The system exists specifically for those who have been hit by circumstances beyond their control.

Can a Doctor Refuse to See You After Bankruptcy?

A common fear is that discharging a debt will result in a total loss of medical care. Massachusetts law and medical ethics guidelines provide a safety net here. While a private physician might choose to terminate a professional relationship if a debt is discharged, they must follow specific protocols. This includes providing notice and ensuring you have access to emergency care during the transition. You won't be blacklisted from the healthcare system. Reading residents have access to a dense network of providers across the North Shore and the greater Boston area. If one relationship ends, our team helps you understand how to transition your care to new providers without interruption. Legal protections ensure that your past financial struggles don't dictate your access to essential treatment.

The Impact on Your Credit Score in Reading

Unpaid medical collections can linger on your credit report for seven years. This drags down your score and limits your housing or employment options in Reading. Filing for bankruptcy provides a definitive end date to this decline. By 2026, the credit landscape in our state will shift significantly. Governor Healey recently announced a comprehensive plan to ensure that Massachusetts protections from medical debt include banning these debts from credit reports entirely. This legislative move recognizes that medical expenses aren't predictive of creditworthiness.

A bankruptcy discharge clears the path now. It allows you to start rebuilding your score immediately rather than waiting for collections to expire. Most clients see a score increase within 12 to 24 months of their discharge because their debt-to-income ratio improves overnight. Choosing medical debt bankruptcy reading ma is often the fastest way to secure a stable financial foundation in the North Shore area. We focus on the results that matter: a clean slate and a return to financial health.

Preparing for Your Filing in Reading: A Local Checklist

Filing for medical debt bankruptcy reading ma requires meticulous organization to ensure every creditor is accounted for and your petition moves through the court without delay. You'll need to compile all outstanding invoices from local providers like Lahey Health and Winchester Hospital. Gather your pay stubs from the last 180 days and tax returns from the previous two years. This documentation allows the U.S. Bankruptcy Court for the District of Massachusetts to assess your financial standing with precision.

The Power of the Automatic Stay

The automatic stay is a powerful legal injunction that instantly stops all collection actions, including lawsuits and wage garnishments, the moment your petition is filed. This protection applies to Reading-based collection agencies and national firms alike. If a debt collector contacts you after you've filed, provide them with your case number and end the conversation immediately. Your legal counsel will handle any further communication to ensure your rights remain protected throughout the process.

Mandatory Steps for Massachusetts Filers

Federal law requires you to complete a credit counseling course from an agency approved by the U.S. Trustee for the District of Massachusetts before filing. Most Reading residents choose online providers to fulfill this 60-minute requirement, which must be completed within the 180-day window preceding your filing date. This step is a prerequisite for your case to proceed and serves as a foundational element of your financial recovery plan.

Your Schedule F is perhaps the most critical document in your filing. You must list every medical provider, from the primary surgeon at Winchester Hospital to the smallest laboratory bill or ambulance service fee. If you miss a single $400 invoice, that specific debt might not be discharged, leaving you personally liable after your case closes. We recommend pulling a comprehensive credit report from all three bureaus to identify any hidden medical collections that have already been sold to third-party buyers.

To ensure your petition is accurate and complete, follow this checklist of local requirements:

- Income Verification: Copies of all pay stubs and sources of income from the last six months.

- Tax Compliance: Filed tax returns for the years 2022 and 2023.

- Medical Records: Detailed billing statements from Lahey Health, Winchester Hospital, and local specialists.

- Counseling Certificate: The official certificate of completion from an approved credit counseling agency.

Taking these steps with disciplined precision sets the stage for a successful discharge of your debts. Our firm acts as a stabilizing force, providing the strategic direction needed to navigate these complex requirements. We focus on results-driven advocacy to secure your financial future.

How MTD Law Protects Reading Families from Collections

Facing a mountain of hospital bills while trying to maintain a household in Reading can feel like an impossible battle. MTD Law intervenes as a dedicated protector for families overwhelmed by the cost of care. We utilize a flat-fee approach for Chapter 7 bankruptcy filings, providing clear financial expectations during a period of uncertainty. This transparent pricing model allows you to secure professional legal representation without the stress of unpredictable hourly billing or hidden costs.

Our firm provides direct advocacy that shifts the burden of communication from your shoulders to ours. When you pursue medical debt bankruptcy reading ma, we take command of the situation immediately. We handle all interactions with collectors and medical billing departments. This stops the constant harassment and allows you to focus on your family's health and recovery. The legal system provides powerful tools like the automatic stay to halt collection actions, and we ensure those tools are used to their full potential for your benefit.

Managing the Middlesex County legal landscape requires specific local expertise. Our deep integration into the Massachusetts court system means we understand the nuances of local filing requirements and trustee expectations. This regional knowledge is vital for a smooth transition through the bankruptcy process. We position your family for a debt-free future by focusing on movement and resolution, ensuring every step of your case is handled with disciplined precision and meticulous attention to detail.

The MTD Law Strategic Advantage

A local Reading attorney understands the specific financial pressures of living in the Greater Boston area. We don't view your case as a simple transaction. Instead, we act as a stabilizing force to bridge the gap between your current financial crisis and permanent security. Our commitment to results-oriented guidance means we prioritize the long-term well-being of your household. We provide the analytical sharpness required to protect your assets while discharging your medical liabilities, acting as a steadfast partner throughout the litigation process.

Schedule Your Free Reading Consultation

Your initial medical debt review is a comprehensive assessment of your financial standing. We examine your eligibility for Chapter 7 or Chapter 13 under the current Massachusetts means test standards. This no-obligation evaluation provides a clear roadmap for your recovery. You'll leave the meeting with a strategic direction and a professional understanding of how to reclaim your financial independence. Take the first step toward relief with a free Reading consultation today.

Take Control of Your Financial Future

Medical bills don't have to dictate your family's future in Middlesex County. Whether you utilize Chapter 7 to wipe out qualifying debts or Chapter 13 to create a manageable repayment plan, the law provides a clear path to stability. Successfully filing for medical debt bankruptcy reading ma requires a precise understanding of local court expectations and state exemptions. MTD Law has advocated for Reading residents since 2008, bringing over 15 years of local experience to every case. We offer flat-fee bankruptcy options to provide the financial clarity you need during a difficult time.

Our firm prioritizes results-driven advocacy in the Middlesex County courts, ensuring your rights remain protected against aggressive collectors. We handle the complex legal details so you can focus on your recovery. It's possible to stop the cycle of debt and secure a lasting resolution. Our team is ready to provide the strategic direction required to transform your financial outlook.

Secure your financial future; schedule your free Reading consultation today.

You don't have to carry this burden alone. We're here to help you reclaim your peace of mind and build a stronger foundation for the years ahead.

Frequently Asked Questions

Is medical debt automatically wiped out in a Reading bankruptcy?

Yes, medical bills are classified as general unsecured debt and are fully dischargeable in a Chapter 7 filing. Under 11 U.S.C. § 523, medical expenses don't fall into the categories of non-dischargeable debt like child support or certain taxes. This means your medical debt bankruptcy reading ma case can effectively eliminate 100% of your qualifying healthcare balances, providing a necessary bridge to financial stability.

Can I keep my house in Reading if I file for medical debt bankruptcy?

Most Reading homeowners protect their primary residence by utilizing the Massachusetts Homestead Act. Under M.G.L. c. 188, you receive an automatic $125,000 in equity protection. By filing a formal Declaration of Homestead at the Middlesex South Registry of Deeds, you can increase this protection to $500,000 per residence. These specific exemptions ensure your family's home remains secure while we resolve your medical liabilities.

Will filing for bankruptcy stop a wage garnishment for medical bills in MA?

Filing for bankruptcy triggers an immediate legal injunction known as the automatic stay. This protection stops all collection activities, including active wage garnishments, the moment your petition is filed with the court. Massachusetts law currently limits garnishments to 15% of your gross wages. Bankruptcy provides the strategic movement needed to halt these deductions and keep your full paycheck for essential living expenses.

Do I have to list all my medical providers in my bankruptcy filing?

You're legally required to disclose every creditor you owe, including local providers like Winchester Hospital or Lahey Hospital. Federal Rule of Bankruptcy Procedure 1007 mandates a complete schedule of all liabilities. If you don't list a specific doctor or clinic, that debt might not be discharged. We ensure every provider is properly notified so your medical debt bankruptcy reading ma filing is comprehensive and final.

How much does it cost to file for bankruptcy in Reading, MA?

The U.S. Bankruptcy Court for the District of Massachusetts sets standard administrative filing fees for all residents. As of late 2023, the court fee for a Chapter 7 case is $338, while a Chapter 13 case costs $313. These fees are mandatory and paid directly to the federal court system. Our firm provides clear guidance on these costs during your initial strategy session to avoid any financial surprises.

Will my neighbors in Reading find out if I file for bankruptcy?

While bankruptcy is a matter of public record, your neighbors won't typically find out unless they specifically search federal court databases. Filings are managed through the PACER system, which requires a registered account and fee for access. Local Middlesex County newspapers don't publish consumer bankruptcy filings. We prioritize your privacy and handle your case with the professional discretion required for sensitive legal matters.

Can I file for bankruptcy on just my medical bills and keep my credit cards?

You cannot legally exclude specific creditors from your filing to keep a particular credit card. Bankruptcy law requires total transparency regarding all financial obligations. Credit card issuers usually close accounts once they receive notice of a bankruptcy filing. This ensures all creditors receive equitable treatment under the law. We focus on this total resolution to build a stronger, debt-free future for your household.

How long does the medical debt bankruptcy process take in Massachusetts?

A typical Chapter 7 bankruptcy case moves from the initial filing to a final discharge in approximately 90 to 120 days. Your mandatory 341 Meeting of Creditors usually takes place between 21 and 40 days after the case begins. If no creditors object within 60 days after that meeting, the court issues the discharge order. This disciplined timeline allows you to resolve your medical debt with predictable precision.

Comments

There are no comments for this post. Be the first and Add your Comment below.

Leave a Comment