We understand that you're looking for a way to resolve your debt without forfeiting your status. Filing for bankruptcy allows you to eliminate the financial vulnerabilities that could otherwise make you a target for coercion or poor judgment. By taking this decisive step, you're demonstrating the proactive financial management that federal adjudicators favor. This article explores how to navigate the disclosure process, satisfy the 13 Adjudicative Guidelines, and ensure your financial past doesn't dictate your professional future.

Key Takeaways

- Understand how Guideline F evaluates financial responsibility and why resolving debt actually reduces your susceptibility to coercion.

- Discover why filing for bankruptcy security clearance Massachusetts is often viewed by adjudicators as a proactive step toward stability rather than a career-ending event.

- Compare the strategic advantages of Chapter 7 and Chapter 13 to determine which filing best demonstrates your "good faith" commitment to federal investigators.

- Learn the precise steps for disclosing your filing on the SF-86 and the critical timing required to maintain transparency with your Facility Security Officer.

- Explore how specialized legal advocacy can protect your professional standing while permanently resolving the financial vulnerabilities that threaten your clearance.

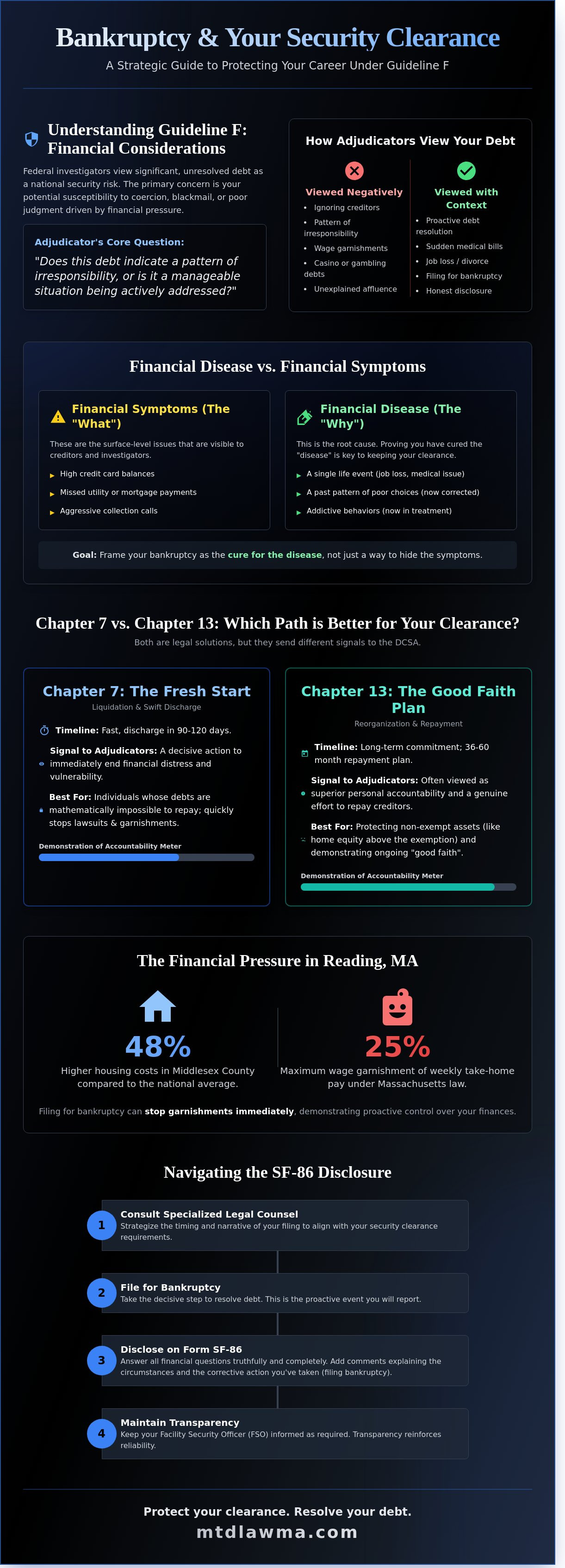

Understanding Guideline F: Why the Government Cares About Your Debt

Guideline F is the federal metric used to evaluate if an individual's financial history poses a security risk. Federal investigators view significant debt as a potential vulnerability that could compromise national interests. The primary concern is your susceptibility to coercion. If you're under extreme financial pressure, you might be tempted to trade classified information for cash to resolve your debts. The Adjudicative Guidelines for Determining Eligibility for Access to Classified Information distinguish between uncontrollable and irresponsible debt. For example, a $75,000 medical bill from an unexpected illness is viewed differently than $75,000 lost at a casino.

The Risk of Unresolved Debt in Reading, MA

Living in Reading presents unique financial challenges that investigators understand. According to 2023 economic data, Middlesex County residents face housing costs that are 48% higher than the national average. This economic pressure can quickly turn manageable debt into a crisis. Adjudicators look for proactive behavior rather than avoidance. Ignoring creditors is viewed more harshly than seeking legal debt relief because it indicates a lack of reliability. Wage garnishments, which can seize up to 25% of your weekly take-home pay under Massachusetts law, create a permanent record of financial instability. Utilizing a bankruptcy security clearance massachusetts strategy early can stop these garnishments and show you're taking charge of your obligations.

Financial Disease vs. Financial Symptoms

You need to distinguish between the root cause of your debt and its symptoms. Adjudicators want to know if your debt resulted from a single life event or a pattern of poor choices. Identifying these causes is essential to maintaining your clearance.

- Financial Symptoms: High credit card balances, missed utility payments, or late mortgage installments.

- Financial Disease: Chronic overspending, lack of budgeting, or addictive behaviors.

A Reading bankruptcy attorney helps frame your narrative by proving the debt is a symptom of an isolated event rather than a disease of character. This strategic positioning often makes the difference between a clearance denial and an approval. Proving that the underlying cause of your debt has been resolved is the most effective way to secure your professional future. Navigating a bankruptcy security clearance Massachusetts case requires this level of detailed, evidence-based advocacy.

Chapter 7 vs. Chapter 13: Which is Better for Your Clearance?

Federal adjudicators evaluating bankruptcy security clearance Massachusetts cases in 2026 prioritize one factor above all others: financial reliability. While both chapters offer a legal resolution to debt, they send different signals to the Defense Counterintelligence and Security Agency (DCSA). A Chapter 7 filing provides a swift discharge, typically within 90 to 120 days, which can immediately stop the "financial distress" trigger that worries investigators. However, Chapter 13 is often viewed as a superior demonstration of personal accountability because it involves a structured repayment plan over 36 to 60 months.

Choosing the right path depends on your specific debt-to-income ratio and the nature of your security role. Adjudicative Guideline F focuses on whether an individual is "frivolous" or "irresponsible." By proactively filing, you demonstrate that you're taking control of the situation rather than letting creditors dictate your financial state. You can consult with a local attorney to determine which filing aligns best with your specific career trajectory.

- Chapter 7: Best for immediate debt elimination and stopping aggressive collection actions.

- Chapter 13: Best for protecting non-exempt assets and showing a long-term commitment to repayment.

- Timing: A Chapter 7 discharge is faster, but a Chapter 13 plan shows ongoing "good faith" during the entire review process.

The Chapter 7 Approach for Reading Residents

For many professionals in Reading, a Chapter 7 liquidation is the most responsible choice when debts become mathematically impossible to pay. It eliminates the risk of future lawsuits or wage garnishments that could lead to blackmail or coercion. In a clearance interview, you must frame this as a decisive action to stabilize your finances. Massachusetts provides robust protections, such as the Homestead Act which protects up to $500,000 in home equity, ensuring you maintain a stable living environment while resolving your liabilities.

The Chapter 13 Repayment Strategy

Chapter 13 acts as a powerful "good faith" signal. It proves you're making a genuine effort to repay creditors through a court-ordered plan. Some federal agencies prefer this strategy because it shows a sustained commitment to meeting financial obligations. This 60-month process requires discipline, which adjudicators often interpret as a sign of high character. It mitigates concerns of financial irresponsibility by providing a transparent, monitored roadmap to solvency. Successfully managing a Chapter 13 plan can actually strengthen your case during a periodic reinvestigation by showing a multi-year track record of fiscal maturity.

Will I Lose My Job? Myth vs. Reality in Massachusetts Bankruptcy

Many professionals in Reading fear that filing for bankruptcy is an automatic career killer. This is a misconception. The statistical reality is that the federal government rarely revokes a clearance solely because of a bankruptcy filing. Data from the Defense Counterintelligence and Security Agency (DCSA) indicates that financial issues are the primary reason for clearance denials, yet these denials typically stem from unresolved debt rather than the legal process of discharging it. By filing for bankruptcy security clearance massachusetts, you're often viewed as taking control of a volatile situation.

Choosing "financial silence" is significantly riskier than seeking legal relief. When you leave debts unpaid and accounts delinquent, you become a potential target for coercion or bribery. This vulnerability is exactly what adjudicators want to avoid. Filing for bankruptcy proves you're addressing the problem head-on. It signals that you've chosen a structured, legal path to stability rather than letting financial chaos persist. It doesn't prove you're irresponsible; it proves you're proactive in protecting your household and your professional standing.

The Role of Transparency and Honesty

Attempting to hide financial distress is more disqualifying than the debt itself. Adjudicators prioritize integrity above almost all else. You must self-report your intent to file before the government discovers it through a routine credit check or periodic reinvestigation. At MTD Law, we help Reading clients prepare for these difficult conversations. We assist in drafting clear, honest statements for investigators that focus on the "why" behind the filing, ensuring your narrative emphasizes honesty over evasion.

Mitigating Factors That Adjudicators Look For

Security clearance adjudicators use the "whole-person concept" to evaluate your case. They look for specific evidence of recovery and stability, such as:

- Completion of mandatory financial counseling sessions required by the bankruptcy court.

- A stable employment history, such as 3 or more years with a single contractor in the Reading or Greater Boston area.

- The passage of time, specifically staying current on all new financial obligations for 12 months or more after your filing date.

These factors demonstrate that your bankruptcy security clearance massachusetts strategy was a one-time necessity caused by circumstances like medical emergencies or divorce, not a pattern of poor choices. We provide the tactical direction needed to highlight these strengths during your review process.

How to Disclose Your Bankruptcy on the SF-86

Reporting a financial setback isn't just about honesty; it's about maintaining control over your professional narrative. When you navigate the intersection of bankruptcy security clearance massachusetts regulations, you must update Section 26 of your SF-86 or e-QIP. Your first move is notifying your Facility Security Officer (FSO) within 30 days of your filing date. This proactive step prevents the appearance of concealment, which adjudicators often view more harshly than the financial distress itself.

Preparation requires gathering specific records from the U.S. Bankruptcy Court for the District of Massachusetts. You'll need your Chapter 7 or Chapter 13 petition, the full schedule of assets and liabilities, and eventually, your final discharge order. Beyond the forms, you must prepare a "Statement of Circumstances." This document shouldn't offer excuses. Instead, it should provide a factual timeline of the events, such as a 2022 medical emergency or a 2023 job loss, that led to the filing.

Working with Your FSO in Reading

Your FSO serves as the primary link between your Reading-based employer and the Defense Counterintelligence and Security Agency (DCSA). It's vital to remember that your FSO doesn't have the authority to revoke your clearance; only the federal adjudicating agency holds that power. They're there to facilitate the flow of information. MTD Law assists clients in reviewing their disclosure paperwork to ensure it's flawless before it reaches the FSO's desk. This precision minimizes the risk of follow-up inquiries that could delay your reinvestigation.

Preparing for the Subject Interview

Expect a background investigator to ask detailed questions about your financial recovery. They'll likely focus on your 12 month post-filing budget to ensure you're living within your means. You can demonstrate "rehabilitation" by presenting your two mandatory financial education certificates required by the court. Showing that you've maintained a 100 percent on-time payment record for all non-discharged debts since your filing date provides the concrete evidence investigators need to see. They're looking for stability, not perfection.

If you're concerned about how your filing impacts your career, contact MTD Law for a strategic consultation to protect your future.

Protecting Your Future with MTD Law in Reading, MA

Choosing the right legal partner in Reading makes the difference between a simple filing and a career-saving strategy. MTD Law focuses on the intersection of debt relief and professional vetting. We navigate the specific nuances of the Essex and Middlesex county legal landscape, ensuring your petition is filed with the precision required by the District of Massachusetts. This local insight allows us to anticipate how a trustee's actions might impact your financial disclosure forms. Our team understands that for professionals in the 01867 area, a legal filing is never just about numbers; it is about maintaining the trust of your employer and the federal government.

Results-Driven Advocacy for Professionals

Professionals in Reading often face unique pressures when debt mounts. We offer a flat-fee service model to ensure financial predictability from day one. Since 2009, our firm has guided over 500 clients through the complexities of bankruptcy security clearance in Massachusetts cases. We don't just file paperwork. We build a tactical defense for your livelihood. Our approach bridges the gap between your current financial distress and a resolution that satisfies both the court and your clearance adjudicators. By providing a clear roadmap, we eliminate the uncertainty that often paralyzes high-clearance employees.

- Predictable flat-fee structures that eliminate hidden costs.

- Direct access to attorneys who understand the Reading and North Shore professional market.

- Strategic filing timelines designed to align with security reinvestigation cycles.

Securing Your Career and Your Peace of Mind

Adjudicative guidelines often view unresolved debt as a greater risk than a proactive bankruptcy filing. By addressing your liabilities now, you demonstrate the financial responsibility required under Guideline F of the National Security Adjudicative Guidelines. This fresh start provides a stable foundation for your next periodic reinvestigation. Managing bankruptcy security clearance massachusetts concerns requires a steady hand and a deep understanding of federal expectations. MTD Law acts as your formidable protector, ensuring your filing is a calculated step toward long-term stability rather than a source of professional vulnerability.

The first step toward resolving your financial stress is a conversation. Schedule your free consultation today with MTD Law. Our confidential sessions provide the clarity you need to protect your career and your family's future.

Take Control of Your Professional Future

Choosing to address your debt isn't a sign of failure; it's a strategic move to protect your federal career. Federal investigators prioritize financial stability and honesty above all else. By filing for bankruptcy, you proactively mitigate concerns under Guideline F and demonstrate that you aren't vulnerable to external pressure. Whether you pursue Chapter 7 or Chapter 13, the goal remains the same: a clear path toward financial recovery and a secured clearance.

Navigating the complex relationship between bankruptcy, security clearance, and Massachusetts requires a partner who understands the local legal landscape. MTD Law offers over 15 years of experience in Massachusetts bankruptcy law, providing specific advocacy for clients throughout Reading, Essex, and Middlesex counties. Our team focuses on the tactical disclosures needed for your SF-86 while shielding your professional reputation from the myths of job loss. You've worked hard to earn your status, and we're here to help you keep it.

Protect your career and your future; schedule a free consultation with MTD Law today.

Financial freedom is within your reach, and your career can emerge stronger than before.

Frequently Asked Questions

Is bankruptcy an automatic disqualifier for a security clearance in Massachusetts?

Bankruptcy isn't an automatic disqualifier for a security clearance in Massachusetts. Federal adjudicators use Guideline F to determine if your financial situation makes you a target for coercion. In 2023, the Defense Office of Hearings and Appeals reported that financial issues were the primary concern in 50% of cases, yet most applicants retained their clearance by showing a proactive resolution. Filing for bankruptcy proves you're taking responsible steps to manage your obligations and mitigate risk.

Should I wait until my clearance renewal to disclose my bankruptcy?

You must report your bankruptcy filing to your Facility Security Officer immediately instead of waiting for your next renewal. Security Executive Agent Directive 3 mandates that all cleared personnel report significant financial changes within 30 days of the filing. Failing to disclose a case in Reading until your 5-year reinvestigation suggests a lack of candor. This omission is often 100% more damaging to your career than the underlying financial debt itself.

Can I get a new security clearance if I have a past Chapter 7 discharge?

You can obtain a new security clearance after a Chapter 7 discharge if you demonstrate 12 to 24 months of financial discipline. Adjudicators evaluate your "whole-person" profile, looking for a consistent record of on-time payments following your case. Statistics from 2022 show that applicants who wait at least two years after a discharge have a much higher success rate. Your ability to maintain a stable budget in Reading after filing proves you're no longer a risk.

How does the government view debt settlement versus bankruptcy?

The government often views bankruptcy more favorably than debt settlement because it provides a legal, court-sanctioned resolution to your debt. While settlement programs often leave you with 1099-C tax liabilities and unresolved accounts, a bankruptcy security clearance massachusetts filing creates a clear, documented end to financial instability. Adjudicators prioritize "good faith efforts" to resolve debt. Filing under Chapter 7 or 13 provides the structured proof they need to mitigate potential security concerns.

What if my debt was caused by a divorce in Reading, MA?

Adjudicators specifically consider financial problems caused by circumstances beyond your control, such as a 2021 divorce in Reading. If your Middlesex County divorce decree resulted in unexpected legal fees or the assumption of 100% of joint marital debt, this qualifies as a mitigating factor under Guideline F. You must provide the court documents and a precise accounting of the impact. Showing that the debt wasn't caused by reckless spending protects your professional standing.

Will my employer in Reading be notified if I file for bankruptcy?

Your employer in Reading isn't directly notified by the court, but your Facility Security Officer will see the filing during routine monitoring. Federal agencies use Continuous Vetting systems that flag new public records within 48 hours of a filing. It's always better to self-report the situation to your supervisor first. Taking the lead on disclosure shows the integrity and transparency that the 13 Adjudicative Guidelines require for all cleared professionals in the state.

How long after my bankruptcy discharge will my credit be considered "stable" again?

Your credit is generally considered stable once you demonstrate 12 months of flawless payment history following your discharge. While a bankruptcy stays on your credit report for 10 years, adjudicators focus on your current financial behavior. Data shows that proactive filers often see their credit scores increase by 50 points within the first year of a discharge. This upward trend proves to the government that you've regained control over your financial life and future obligations.

Does filing for Chapter 13 look better to an adjudicator than Chapter 7?

Neither chapter is inherently better, but Chapter 13 shows a structured 3 to 5 year commitment to repaying a portion of your debt. Adjudicators often appreciate the "good faith" effort involved in a court-ordered repayment plan. However, Chapter 7 is also acceptable if it provides the "fresh start" needed to end 100% of your delinquent accounts. The most important factor is that you've stopped the financial instability that makes you vulnerable to outside influence.

Comments

There are no comments for this post. Be the first and Add your Comment below.

Leave a Comment